Telematics has moved far beyond its early role as a mileage tracker. It’s now at the heart of a technological shift that’s reshaping how insurance works. Modern vehicles are essentially smart devices on wheels—connected, data-rich, and constantly communicating. By 2030, it’s expected that nearly half of a car’s total value will come from its internal software and electronics. For insurers, this opens new possibilities beyond traditional usage-based models.

Telematics 2.0 introduces smarter systems powered by artificial intelligence (AI) and the Internet of Things (IoT). This next wave enables more than just monitoring—it allows for real-time risk management, predictive analytics, and personalized pricing, all while improving how insurers engage with customers.

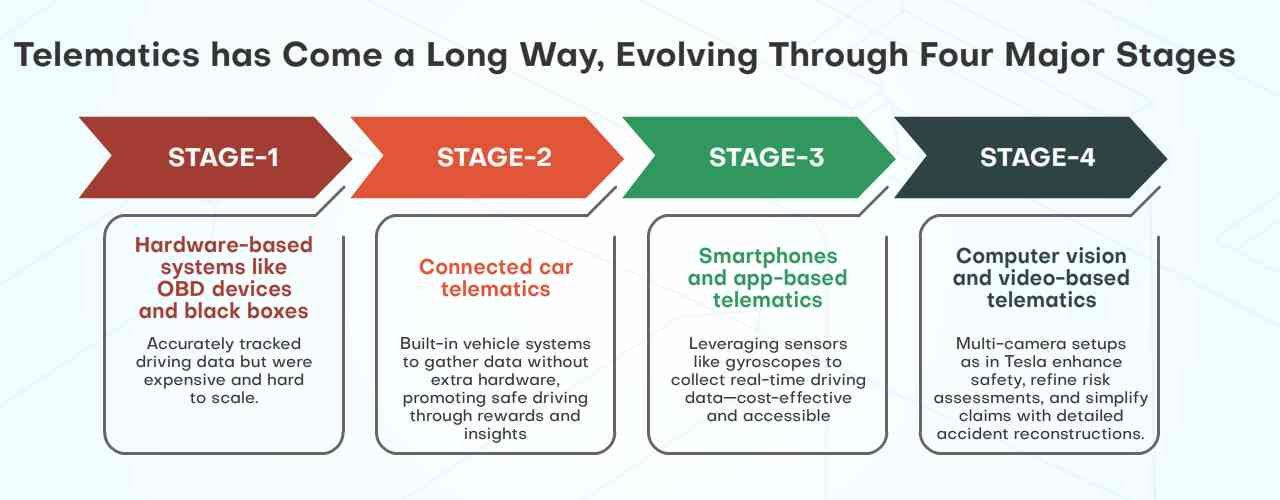

From Data Collection to Context-Driven Insights

Early telematics insurance focused on basic driver metrics—how fast people drove, how often they braked, and how many miles they traveled. Today, it’s not just about how someone drives, but where, when, and under what conditions.

Telematics 2.0 brings in a new layer of context. Factors like road conditions, weather, traffic, and time of day are being added to risk models. This gives insurers a more accurate and real-time view of potential risks, allowing them to create dynamic pricing structures that can adapt to changing environments and driver behaviors.

Predictive Maintenance: More Than Just Risk Reduction

Predictive maintenance, once mainly used in fleet operations, is now gaining ground in personal insurance. With access to live diagnostics and real-time vehicle data, insurers can spot potential problems before they lead to breakdowns or accidents—saving both the customer and the company money.

Munich Re has developed a solution that allows insurers to integrate predictive maintenance directly into their offerings, either through a standalone app or a flexible SDK that fits into their current systems. These tools give insurers detailed insights into vehicle performance and allow for more proactive risk management.

As machine learning and IoT tech become more advanced, insurers can now predict mechanical issues with greater precision. Companies like State Farm are using this capability to offer timely maintenance suggestions based on driving behavior and diagnostics—helping customers avoid costly repairs while reducing claims. Some insurers have reported up to 30% better accuracy in risk assessments and a 20% drop in accident rates.

Gamification & Behavioral Science: Driving Change Through Engagement

Usage-based insurance (UBI) already rewards safe driving, but Telematics 2.0 takes it further by using behavioral science to encourage long-term change. Through gamification—think points, badges, rewards, and leaderboards—insurers can actively influence how people drive, not just monitor it.

Research from the University of Guelph has shown that gamified insurance programs, especially among younger drivers, significantly increase user engagement and program enrollment. Root Insurance uses these strategies to tailor pricing based on behavior, resulting in fewer claims and safer drivers. Their approach has led to a 15% decrease in claim frequency.

Cambridge Mobile telematics insurance found that integrating gamification and real-time feedback reduced accident risks by up to 40%. These results highlight how telematics can go beyond cost savings and become a tool for improving road safety.

Expanding Value Through Ecosystem Partnerships

One of the most exciting aspects of Telematics 2.0 is its potential outside of insurance. By partnering with automakers, city governments, and retailers, insurers can make driving data work in broader, smarter ways.

For instance, sharing anonymized driver data with city planners can help improve infrastructure and traffic flow. Audi’s Traffic Light Information system already uses real-time vehicle data to optimize signal timing, helping reduce congestion. On the retail side, insurers can offer customer perks based on driving habits—like Progressive’s Snapshot program, which ties safe driving to personalized discounts and partner deals.

These partnerships don’t just add value for customers—they position insurers as key players in a connected, data-driven ecosystem.

Making Big Data Work with AI

With millions of data points flowing in from telematics insurance devices, AI and machine learning are essential for turning raw data into meaningful insights. These tools help insurers identify trends, detect fraud, and score risk more accurately and in real time.

This level of automation allows insurers to respond faster to claims, offer better underwriting, and create smarter policies. It also opens the door for truly personalized experiences—tailored coverage, real-time updates, and proactive service that keeps customers safer and more satisfied.

What’s Ahead for Telematics?

Several trends are shaping the next phase of telematics in insurance:

-

Connected Cars and 5G: Faster data transfer and always-connected vehicles will allow real-time updates to policies, claims, and driver support.

-

Embedded Insurance: Telematics is being integrated directly into the car-buying or leasing process, providing seamless coverage from the start.

-

Environmental Tracking: Future telematics tools may track carbon emissions, promoting eco-friendly habits and aligning insurers with sustainability goals.